How conventional utilities may drive the solar energy transition

Ken Silverstein

More than 95 percent of consumers will still be connected to the centralized network for the foreseeable future. But it won’t diminish the trend toward distributed generation – and the attempts by both unconventional parties and power companies from getting into related businesses.

(December2012) KC Electric Association expects soon to finalize installing a Sensus FlexNet network and iCon A electric meters to serve about 4,000 residential and small commercial members across a 5,000-square-mile territory in rural Colorado. Itron and C3 Energy formed an alliance to integrate and jointly market an energy management solution to North American utilities. And others...

Byline:

By Jack Azagury, Walt Shill, and Ted Walker

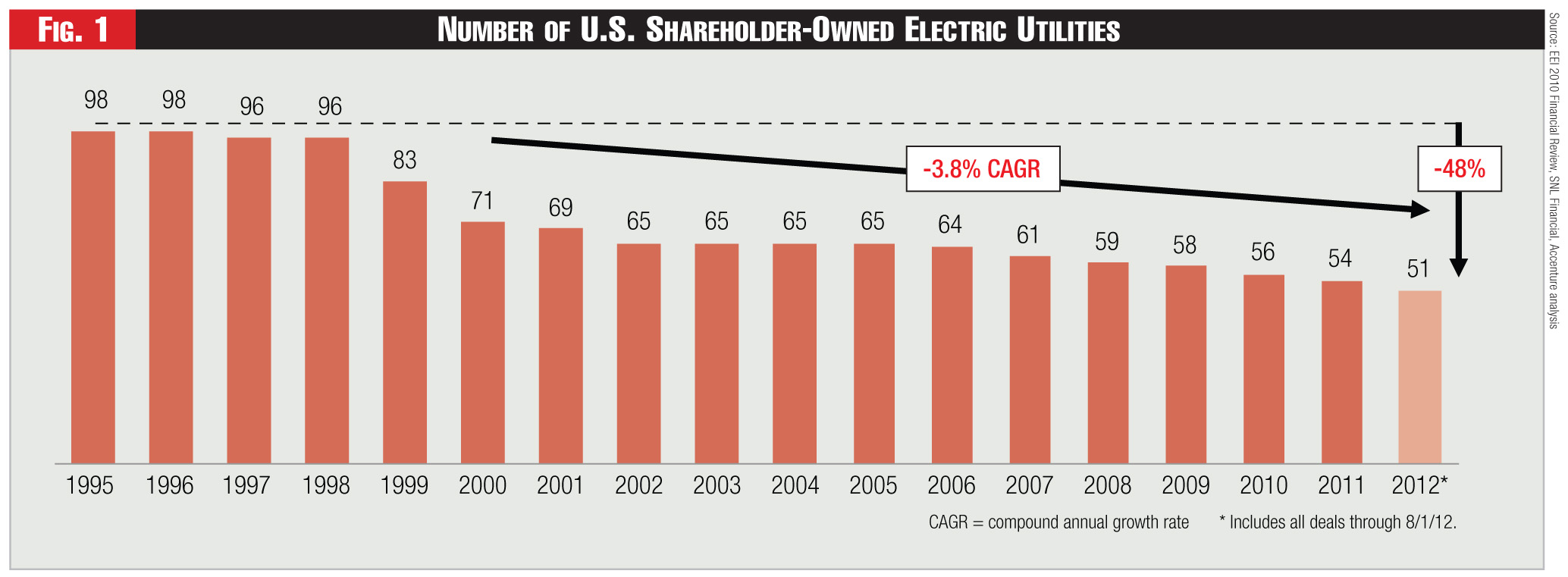

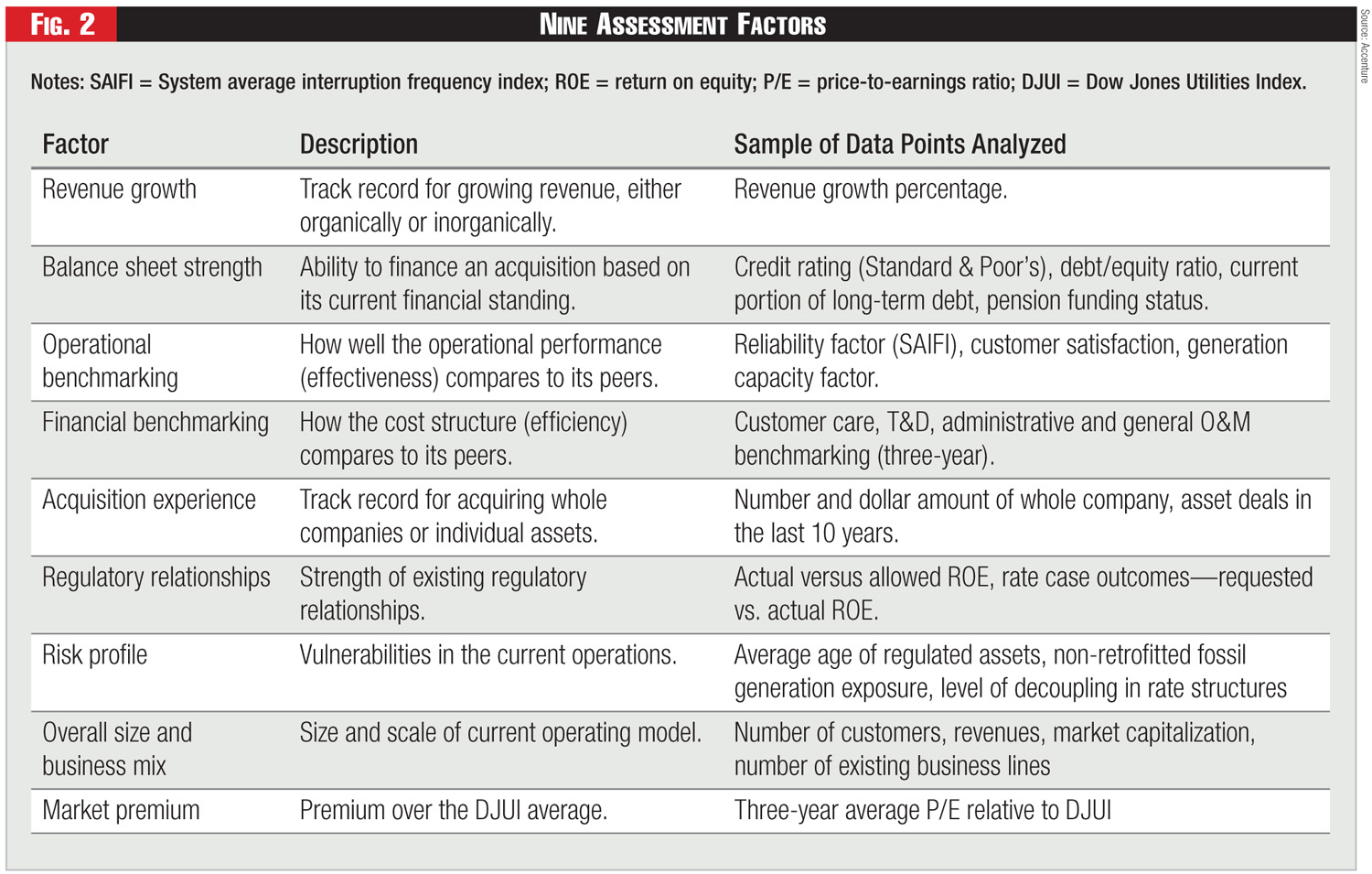

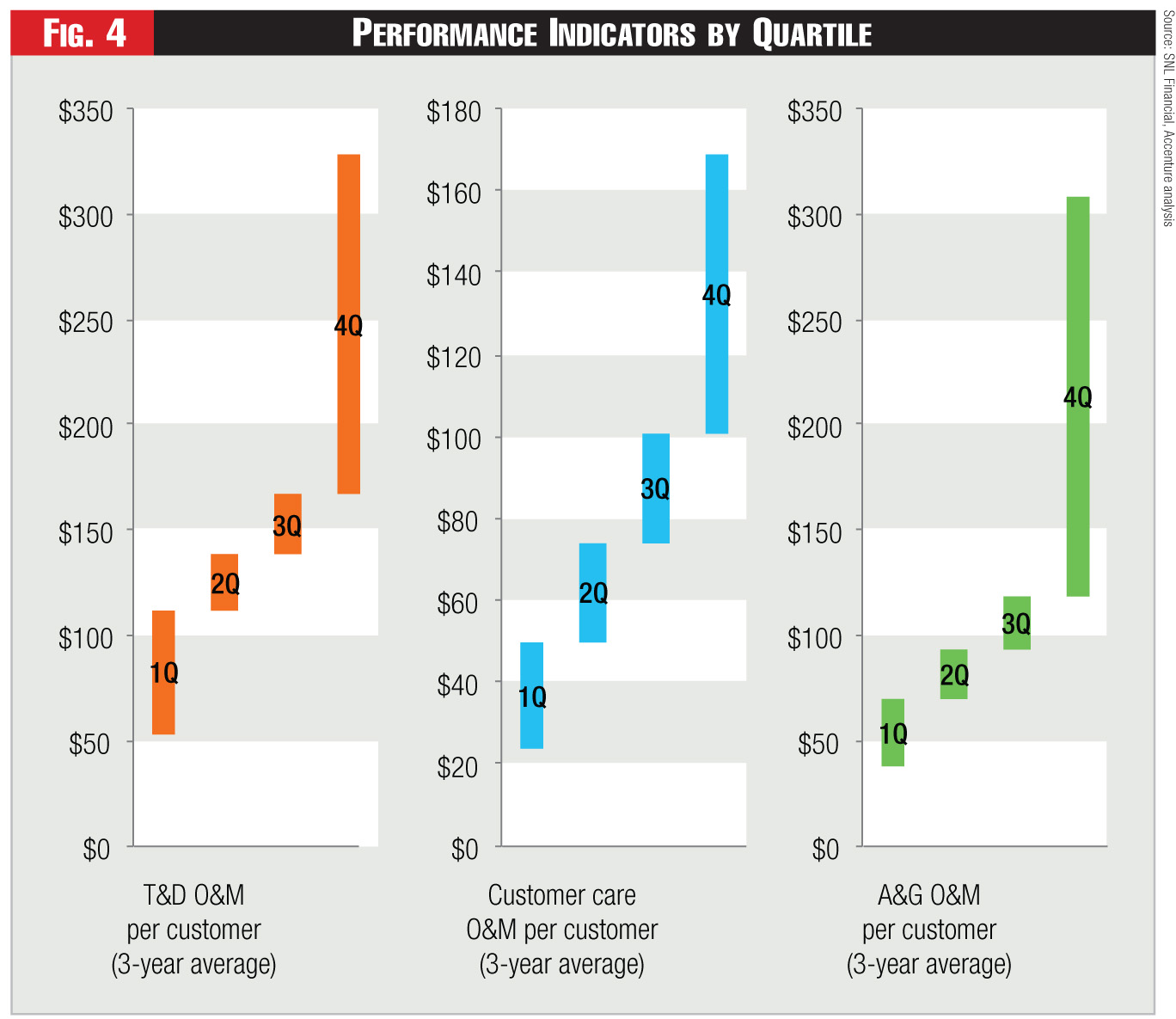

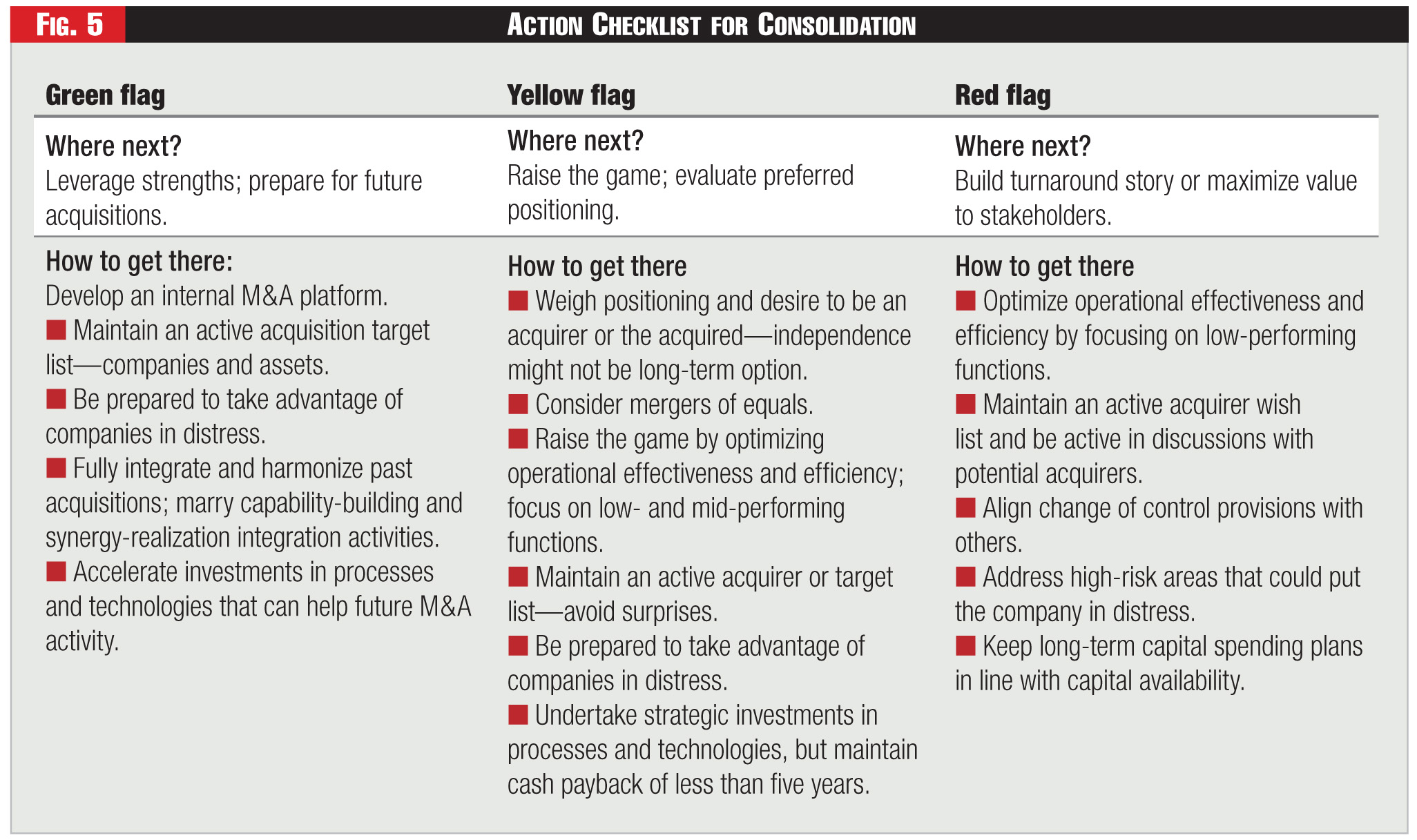

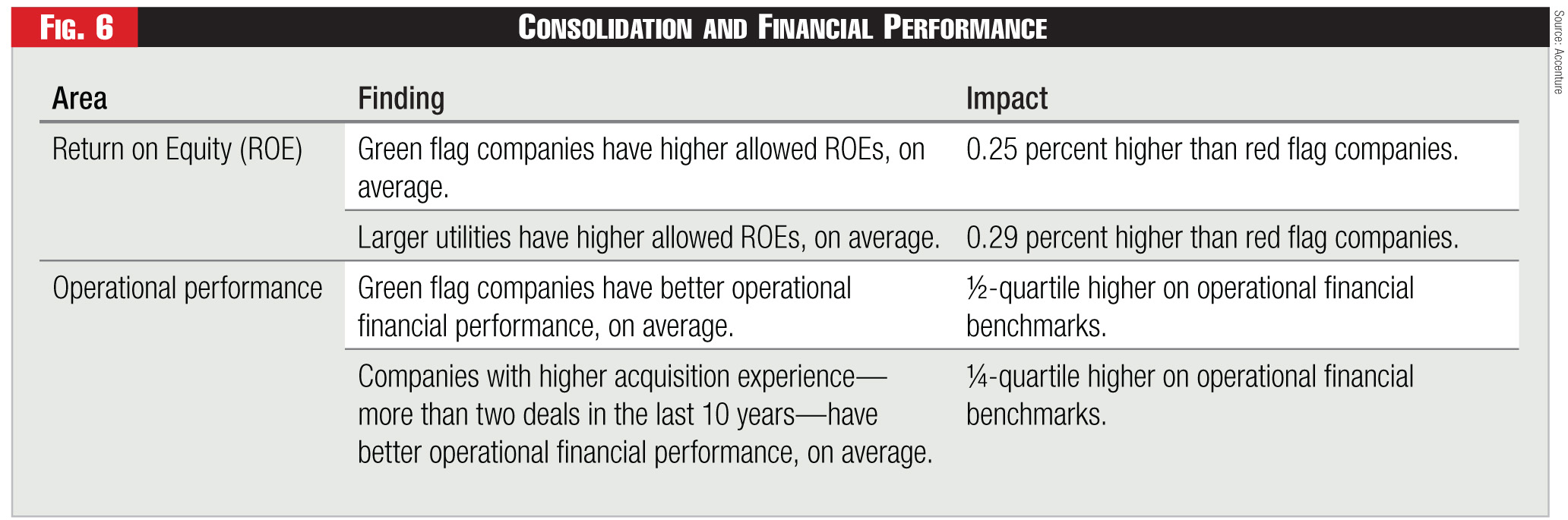

The industry’s slow-and-steady pace of mergers seems to be picking up speed, as larger and well-positioned players overtake smaller and weaker targets. Realizing the greatest value from consolidation requires companies to assess their strengths and weaknesses and focus on performance improvement—both before and after a deal gets done.

Author Bio:

Jack Azagury (jack.azagury@accenture.com) is Accenture’s North American Management Consulting lead for the resources industries, and Walt Shill (walt.shill@accenture.com) is global senior director at the company. Ted Walker (ted.h.walker@accenture.com) is a senior manager in the Accenture Utilities Strategy group. The authors acknowledge contributions from Jan Vrins, Accenture Utilities Management Consulting group, and Jason Allen, Accenture Research.

Positioning to win in the contest for scale.

(September 2012) Our annual financial ranking shows some remarkable shifts among the industry’s shareholder value leaders. Despite flat demand and low commodity prices, investor-owned utilities are investing heavily in capital assets. Investment discipline and operational excellence distinguish leaders on the path to financial performance.

Category:

The <i>Fortnightly 40</i> Best Energy Companies

Author Bio:

Michael T. Burr is Fortnightly’s editor-in-chief. He acknowledges the editorial contributions of the C Three Group and Accenture.

A challenging year brings a change in the rankings.

Channel strategies for the new energy consumer

Greg Guthridge, Nicholas Handcock, and Qaid Damji, Accenture

Self-service is the key to reducing operational costs and providing customers with the interactive and mobile tools they want -- and increasingly that they expect.

Asset options in a fast-moving market.

David J. Quiram, Andre Begosso and Robert Laurens, Accenture

Mergers and acquisitions can help companies balance their asset portfolios and improve their financial strength. But economic and regulatory forces are driving more buyers into the market, and the demand for attractive targets might soon outstrip the supply.

Demand Curve Points to Rising Prices

Dan Krueger, Andre Begosso and Curtis Bech

Even with recent large natural gas discoveries and strong inventories, the supply of natural gas isn’t elastic enough to handle significant demand increases. Rising gas prices will push coal back into the money despite coal plants’ high costs to comply with EPA regulations.